The Green Sheet Online Edition

May 12, 2025 • 25:05:01

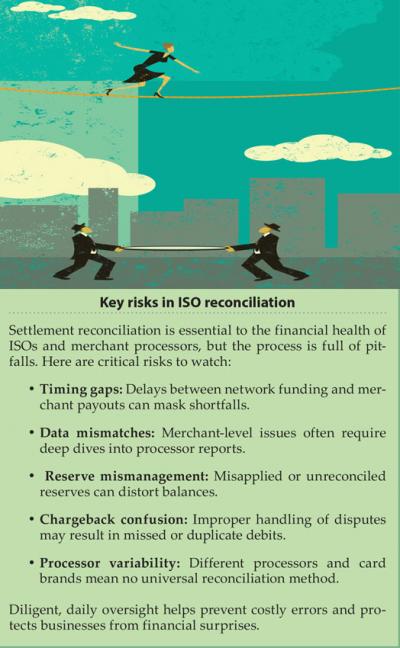

Balancing act: The high stakes of ISO settlement reconciliation

Visa and Mastercard recognize an acquirer based on its Bank Identification Number (BIN) and Interbank Card Association Number (ICA). Money is moved between the issuer and acquirer through each card network's bank in accordance with the instructions from their respective processors.

Wholesale ISOs and processors receive funds deposited daily via a wire from the respective card network's bank, net of fees, returns and chargebacks. Reconciliation occurs daily and ideally without incidence, but when you consider the number of card brands and the myriad GOESINTOs and GOESOUTSOFs, it's impressive that there are not more out of balance incidences.

How can I be overdrawn when my debit card is still valid?

Many ISOs have lost fortunes—and their businesses—because they did not properly reconcile their settlement or reserve accounts. Wholesale ISOs and processors are particularly vulnerable because they often hold excess cash due to the timing difference between when their settlement accounts are funded by the card networks and when their merchants are paid.

If you walk around with an extra $20 million in your bank account, you won't bounce a check until that $20 million is withdrawn even if you do not balance your checkbook. That issue caused some ISOs difficulties over the years.

If you think about an ISO's settlement account, it is typically funded on day-one and then the merchant is paid on day-two less fees, returns, chargebacks and reserves. Because of the delay in merchant payout and the accumulation of reserves, the merchant processor will typically have a positive net settlement account. (If the portfolio is all set to month-end discount, there will be a deficit toward the latter half of the month.)

Regardless, this work in process, needs to be reconciled daily or else the settlement account will not properly reflect the available balance. This very oversight is what has been so costly to so many merchant processors and ISOs.

To further illustrate the complexity, merchant processors have many card types: Visa, Mastercard, American Express, Discover and every available PIN debit network. Each has its own set of reconciliation reports.

Typically, a merchant processor won't consume the reconciliation reports from each card network but will instead rely on the reporting as provided by its processor. Some details will, however, still need to be researched directly with the associated card network if billing items are not routed through the processor.

It was my understanding there would be no math

In addition to complexities associated with each card network, most processors will allow their merchants to receive funding at different time periods. Large merchants with quality credit may have no delay on their funds. Smaller merchants may have a one-day delay, and higher risk merchants may have a three- or five-day delay.

Moreover, some merchants may have a percentage of their processing earmarked to a specific merchant reserve. Both the work-in-process funds and merchant-specific reserves need to be reconciled.

As mentioned, some merchants pay a daily discount. Further, dispute items must be accounted for and again, by card network. Chargebacks are netted against an acquirer's funding wire, and the merchant processor needs to determine if the merchant is in turn debited or if the funds are suspended while an item is adjudicated.

Exception item transactions must be monitored daily to ensure any item that was debited is either correspondingly assessed to a merchant or rejected back to the issuer ... and within the prescribed time frames. Again, reconciliation is not automatic, and rejects and on-the-floor items are commonplace and require manual intervention.

A real-life balancer

Karen Currie makes her living providing reconciliation services for merchant processors and sponsor banks. She works with all the common processors and is well versed in their recommended reconciliation custom and practices. I asked Karen three questions as follows:

- What is the most difficult part of daily/monthly reconciliation?

It can be very tedious and time consuming. Some days run smoothly; but when there is a problem or reject issue, there are thousands of reasons, and each of these could have a different resolution to make the settlement account whole.

- What is most misunderstood regarding reconciliation?

Settlement data is provided at a portfolio level, not a merchant level. When there is a merchant-level issue that does not resolve itself, any research involves assistance or intervention from the processor to drill down a problem to a specific merchant or merchants.

Many times we know there is a problem but need to work with the processor to determine if it is a global issue or something merchant specific.

- When is the best time to hire someone to handle settlement reconcilement?

Whether it be someone like me or an internal person at your company, you should have someone involved in reconciling the settlement account when live testing begins (before any merchants are boarded).

And, if you are establishing a new relationship with a processor, it can be beneficial to have someone involved with the implementation calls, so that funding protocols are set up correctly before going live.

Karen's contact email is karen@pmtsconsult.com

I'll close this article by emphasizing her last point. Processors have core settlement reports, but the reconciliation process will differ depending on the set-up instructions provided.

Because the set-up instructions are set prior to any processing, they are sometimes not fully understood, but once set, they are often immutable and dictate the daily processes required to reconcile and settle a portfolio. Some of these decisions are critical and need to be fully contemplated.

Reconciliation issues will occur. Understanding the process and underlying reporting is key to resolving these issues in order to prevent larger and more systemic problems.

As founder of Humboldt Merchant Services, co-founder of Eureka Payments, and a former executive for such payments innovators as WePay, a division of JPMorgan Chase, Ken Musante has experience in all aspects of successful ISO building. He currently provides consulting services and expert witness testimony as founder of Napa Payments and Consulting, www.napapaymentsandconsulting.com. Contact him at kenm@napapaymentsandconsulting.com, 707-601-7656 or www.linkedin.com/in/ken-musante-us.

Notice to readers: These are archived articles. Contact information, links and other details may be out of date. We regret any inconvenience.